The FCA has recently ended consultation (CP21/9), which covered changes to UK MiFID’s conduct and organisational requirements. The paper deals with the relaxing of certain obligations relating to investment research and execution reporting but does not impose any additional obligations on firms. We are expecting a policy statement at some point in the second half of 2021, with a likely implementation date in early 2022 at the earliest but as of yet this has not been clarified by the FCA.

Who Will be Affected?

- Investment Firms and Market Operators in the UK;

- Banks and Collective Investment Schemes providing investment services;

- Investment Advisors and Article 3 Firms (MiFID);

- Persons providing research that are not authorised by the FCA; and

- Users of services listed above or use services for research purposes.

The Issues

Investment Research

Investment research is crucial in providing investors understanding of the market they operate within and historically brokerage firms have ‘bundled’ research costs for shares with transaction commission. MiFID II introduced requirements to separate these charges, resulting in firms either having to pay for the research themselves or agreeing a separate research charge with clients. This looked to improve accountability over costs passed to customers and improve price transparency for research and execution services.

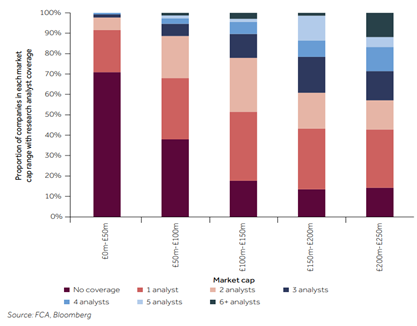

MiFID II requirements, however, did not take market capitalisation and size of firm into account when applying these requirements, meaning the policy is a ‘one size fits all’ not offering exemptions for different parts of the equity market. Some parts, e.g. Small and Medium sized Enterprises (SMEs) have been subject to these regulations, even though these firms are less likely to cause harm through bundling the two services. As a result of MiFID II smaller firms have been left with limited or no coverage for research as seen in Figure 1:

Taken from the CP21/9 report showing ‘Level of research analyst coverage based on company market cap’

This clearly shows that the lower the level of market capitalisation, the lower the investment research coverage is within these firms due to the cost of research needing to be covered by these firms who cannot afford, or find it hard justify, such costs. Research conducted by the FCA shows that 28% of UK listed companies have no research coverage whatsoever.

Best Execution

MiFID II also introduced new reporting requirements, RTS 27 for firms executing and transmitting client orders and RTS 28 to make public information on execution quality and order routing. The policy goals of these requirements were to improve investor protection and transparency in how firms execute client orders. Policy work by the FCA has found that both RTS 27 and 28 have not achieved their initial policy goals and in fact the new reports were not being utilised by market participants making their production effectively pointless. The information within the reports by market participants was seen as not being useful and did not aid in their decision making.

The Solutions

Investment Research Proposal

The FCA has reviewed the inducement rules for research to look at reducing the barriers to producing research under MiFID II, in particular for SME research. The two ways identified to start to tackle this are exempting both SME research and Fixed Income, Currencies and Commodities (FICC) research from the current unbundled MiFID II requirements.

The proposition by the FCA is to create exemptions for SME research for firms under £200 million market capitalisation to reflect and address the potential market failure of low-level coverage in research. This £200 million threshold will be assessed for 36 months preceding the provision of the research as long as it is offered rebundled or for free. This exemption will also be extended to research in connection to FICC instruments and the investment strategies that will rely on such research.

Independent research providers will also be exempt under these propositions as long as they are not engaged in execution services and are not part of a financial services institution. This is to aid in the development of competition within the market for the production of research for the betterment of the investors, as they provide an alternative source of information for investment firms. Similarly, openly available research from third parties to any firm wishing to receive it or the general public will also be exempt under these propositions.

Best Execution Proposal

Due to RTS 27 and 28 not being utilised by market participants, alongside their costly and time-consuming nature of production, the FCA is proposing the deletion of these obligations. This will come alongside changes to the handbook namely:

- Removing COBS 11.2A, 11.2B and 11.2C.

- References made to firms having to take account of data produced under RTS 27, replaced by references to taking account of relevant data or other internal analyses.

- Reference to RTS 27 obligations for Multilateral Trading Facilities, Organised Trading Facilities and Systemic Internalisers (MAR 5, 5A and 6).